Market Overview

The Automotive Exhaust Gas Turbochargers Market plays a crucial role in improving engine performance, enhancing fuel efficiency, and reducing emissions across passenger and commercial vehicles. As per Redline Pulse, turbochargers are increasingly used to support engine downsizing trends while maintaining power output, making them essential in modern internal combustion engine platforms under tightening emission regulations.

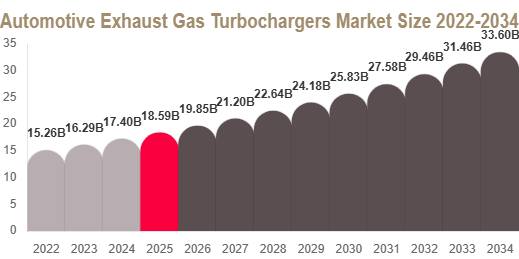

Automotive Exhaust Gas Turbochargers Market Size

Market Size 2025

The Automotive Exhaust Gas Turbochargers Market size is estimated at USD 18.75 billion in 2025, driven by rising demand for fuel-efficient vehicles and stricter emission norms.

Market Size 2034

By 2034, the market is projected to reach USD 33.60 billion, supported by continued integration of turbocharging technologies across global vehicle production.

CAGR (2025–2034)

The market is expected to grow at a CAGR of 6.8% during 2025–2034, reflecting steady expansion across automotive applications.

Market Drivers

Stringent Emission Regulations

Rising global emission standards are pushing automakers to adopt turbochargers to improve combustion efficiency and reduce carbon output. Turbocharging technology helps engines meet regulatory requirements without sacrificing performance.

Growing Demand for Engine Downsizing

Automakers are increasingly adopting smaller engines combined with turbochargers to achieve better fuel efficiency while maintaining high performance. This trend is especially strong in passenger vehicles.

Rising Demand for High-Performance Vehicles

Consumer demand for vehicles with better acceleration and power output is boosting the adoption of turbocharging systems across both gasoline and diesel engines.

Market Challenges

High Cost of Advanced Turbocharging Systems

Advanced technologies such as electric turbochargers and variable geometry systems increase production costs, limiting adoption in cost-sensitive markets.

Wear and Maintenance Issues

Turbochargers operate under extreme temperature and pressure conditions, leading to potential wear and higher maintenance requirements over time.

Limited Adoption in Entry-Level Vehicles

In budget vehicle segments, manufacturers often avoid advanced turbo systems due to cost constraints, limiting market penetration.

Market Segmentation

By Technology

Variable Geometry Turbochargers

This segment dominates with a 48.3% share in 2025 due to superior efficiency, adjustable airflow control, and strong adoption in diesel engines.

Wastegate Turbochargers

These are widely used in standard engine configurations due to cost-effectiveness and reliable performance.

Electric Turbochargers

This segment is the fastest growing, driven by improved response time, elimination of turbo lag, and rising adoption in hybrid and performance vehicles.

By Vehicle Type

Passenger Vehicles

This segment holds a 54.6% share in 2025 due to high production volumes and increasing demand for fuel-efficient vehicles.

Commercial Vehicles

Expected to grow steadily due to rising logistics demand and need for durable high-performance engines.

By Fuel Type

Diesel

Diesel engines dominate with a 57.9% share in 2025 due to widespread use in commercial transport and heavy-duty applications.

Gasoline

This segment is growing due to increased adoption of turbocharged gasoline engines in modern passenger vehicles.

Key Players Analysis

Garrett Motion

Garrett Motion is a leading global player specializing in advanced turbocharging technologies, including electric turbo systems for modern vehicles.

BorgWarner Inc.

BorgWarner focuses on innovative turbocharging and electrification solutions to improve engine efficiency and reduce emissions.

Cummins Inc.

Cummins develops high-performance turbocharging systems widely used in heavy-duty and commercial vehicles.

Mitsubishi Heavy Industries

The company is known for its advanced turbocharger systems used in automotive and industrial applications.

IHI Corporation

IHI specializes in turbocharging technology with strong expertise in variable geometry systems.

Continental AG

Continental provides integrated automotive systems including advanced engine boosting technologies.

Bosch

Bosch contributes through electronic systems and components supporting turbocharger efficiency and control.

Honeywell International Inc.

Honeywell is a key provider of turbocharger systems and performance-enhancing automotive solutions.

ABB Ltd.

ABB focuses on advanced engineering solutions supporting turbo machinery and industrial applications.

Mahle GmbH

Mahle develops engine components and thermal systems supporting turbocharged engine efficiency.

Regional Analysis

North America

North America holds a 32.4% share in 2025 due to strong demand for high-performance vehicles and widespread adoption of turbocharged engines.

Europe

Europe accounts for 27.1% share, driven by strict emission regulations and strong focus on fuel efficiency and sustainable automotive technologies.

Asia Pacific

Asia Pacific is the fastest-growing region with a CAGR of 7.6%, supported by rising vehicle production, urbanization, and increasing demand for fuel-efficient engines.

Middle East & Africa

Growth is supported by expanding transportation and construction activities requiring durable and high-performance engines.

Latin America

Gradual growth is driven by increasing vehicle production and rising adoption of turbocharged engines in passenger vehicles.

Conclusion

The Automotive Exhaust Gas Turbochargers Market is expected to show steady growth through 2034, driven by tightening emission norms, engine downsizing trends, and rising demand for performance vehicles. Despite challenges such as high system costs and maintenance requirements, technological advancements like electric turbochargers are expected to unlock new growth opportunities.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-exhaust-gas-turbochargers-market/request-sample